November 2025 Portfolio Construction

Alfred Lam, MBA, CFA, Senior Vice-President & Chief Investment Officer, CI GAM | Multi-Asset Management

Richard J. Wylie, MA, CFA, Vice-President, Investment Strategy, CI Assante Wealth Management

Interest rates begin to fall again

Canadian economy looks for support from lower interest rates

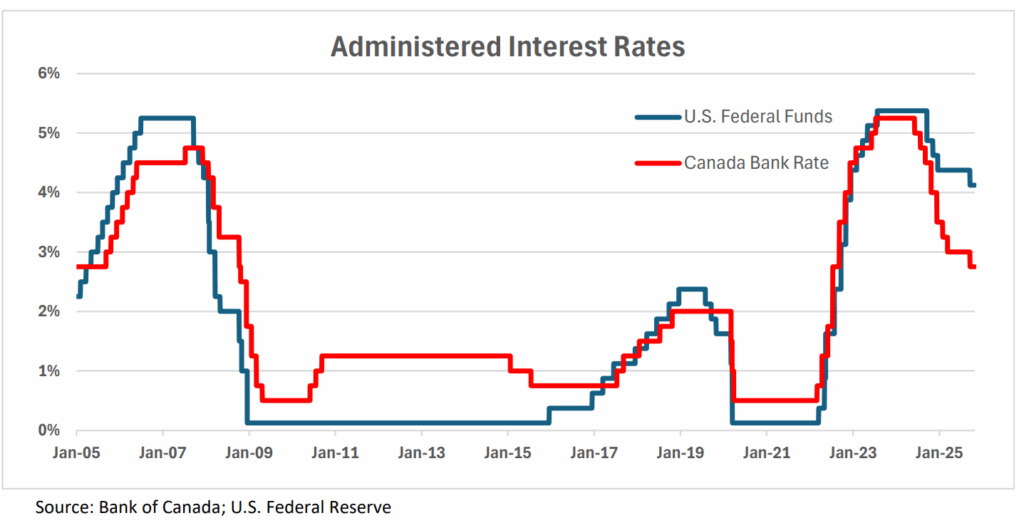

The Bank of Canada announced that it was lowering administered interest rates by 25 basis points (a basis point is 1/100th of one percent) at the conclusion of its September 17, 2025, monetary policy meeting. As can be seen in the accompanying graph, this was the first move by the Bank since March 12 of this year. On the same day, the U.S. Federal Reserve (Fed) cut interest rates by the same amount. However, this was the first interest rate cut by the Fed since December 18, 2024.

Domestically, the range for overnight borrowing was set at 2.50% to 2.75%, with the official benchmark Bank Rate at 2.75%. Stateside, the target for the federal funds rate was set in the range of 4.00% to 4.25%. It is not surprising that policy rates are being set lower in Canada as continued weakness in both business investment and productivity has accompanied a softening in the broader employment picture since the first move to provide a greater separation between administered interest rates in Canada and the U.S. on June 5, 2024.

This “spread” has gone from 12.5 basis points at that juncture to 137.5 basis points. Far greater economic uncertainty prevails in Canada. International trade disruptions continue to make headlines, but perhaps of greater concern to the Bank of Canada is the recent move up in inflation. The CPI was up 2.4% (year over year) in September, well above the 1.9% pace posted in August. In addition, the three Bank of Canada core inflation measures remained elevated in September, ranging from 2.7% to 3.2%. It remains to be seen how much lower rates can go with inflation moving in the opposite direction.

U.S. economy remains strong

The U.S. Bureau of Economic Analysis announced that real gross domestic product (GDP) expanded by 3.8% (quarter over quarter annualized) in the second quarter of 2025. This is the “third estimate” and represents an upward revision to the 3.3% figure that was previously reported. In the first quarter of 2025, real GDP contracted by 0.6% (revised from 0.5%) on the same basis. The most recent reading was the strongest since the third quarter of 2023 (+4.7%) and was the eleventh gain in the previous twelve quarters. The update primarily reflected a downturn in imports and an acceleration in consumer spending that were partly offset by a downturn in investment. In either case the year-over-year growth rate of 2.1% suggests a healthy economy.

Longer View

Investor attention has been focused on global tariffs initiated by President Donald Trump. While this is a significant development, it is unlikely to have the same long-term impact as innovation on our lifestyle, economy, and stock market performance over the next decade. Artificial intelligence will not only strengthen existing ecosystems but also has the potential to create entirely new ones. In a rapidly changing world, the most dangerous investment strategy is one based on a “rear-view mirror” mindset.

Important Disclaimers

The information contained herein consists of general economic information and/or information as to the historical performance of securities, is provided solely for informational and educational purposes and is not to be construed as advice in respect of securities or as to the investing in or the buying or selling of securities, whether expressed or implied. This document may contain forward-looking statements. These statements reflect what the authors believe and are based on information currently available to them. Forward-looking statements are not guarantees of future performance. We caution you not to place undue reliance on these statements as a number of factors could cause actual events or results to differ materially from those expressed in any forward-looking statement, including economic, political and market changes and other developments. Neither CI Private Wealth nor its affiliates, or their respective officers, directors, employees or advisors are responsible in any way for any damages or losses of any kind whatsoever in respect of the use of this document or the material herein. CI Private Wealth is a division of CI Private Counsel LP CI Assante Wealth Management is a registered business name of Assante Wealth Management (Canada) Ltd. CI GAM | Multi-Asset Management is a division of CI Global Asset Management. CI Global Asset Management is a registered business name of CI Investments Inc. This document may not be reproduced, in whole or in part, in any manner whatsoever, without the prior written permission of CI Private Wealth. © 2025 CI Private Wealth, a division of CI Private Counsel LP. All rights reserved. 25-10- 1517800 (10/25)