December 2025 Portfolio Construction

Alfred Lam, MBA, CFA, Senior Vice-President & Chief Investment Officer, CI GAM | Multi-Asset Management

Richard J. Wylie, MA, CFA, Vice-President, Investment Strategy, CI Assante Wealth Management

Canadian inflation stabilizes – for now

Carbon tax issues still pose an inflationary risk

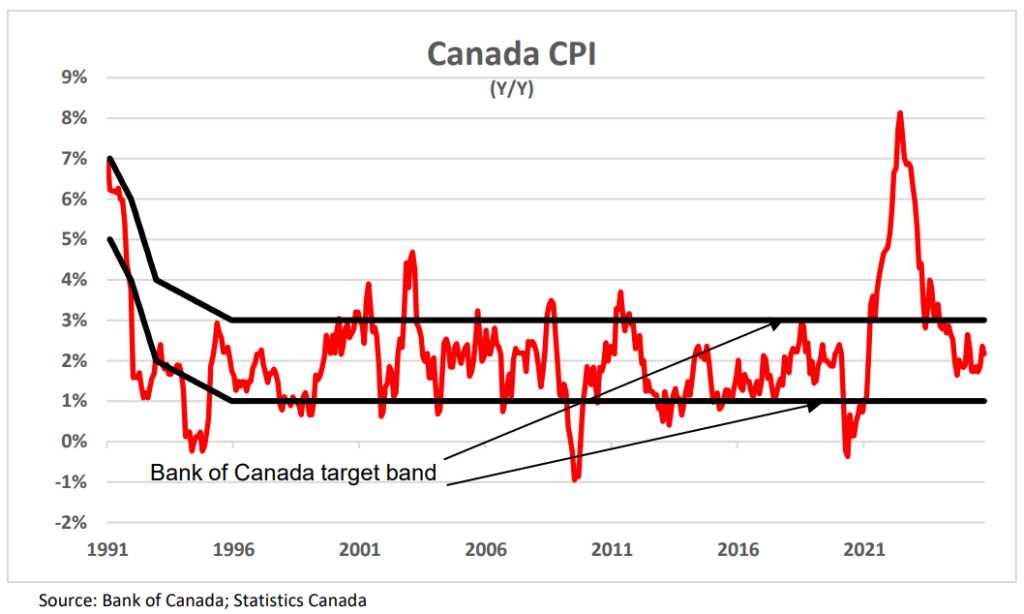

Canada’s federal government temporarily cut the carbon tax on consumers to zero in April of 2025. The effects on the consumer price index were seen immediately. At the time, Statistics Canada revealed that “gasoline led the decline in consumer energy prices, falling 18.1% year over year in April, following a 1.6% decline in March. The price decrease in April was mainly driven by the removal of the consumer carbon price. Year over year, prices for natural gas fell 14.1% in April, after a 6.4% gain in March. The removal of the consumer carbon price contributed to the decline in April.” As can be seen in the accompanying graph, the annual pace of overall inflation has remained inside a 1.7% to 2.4% range since that time. However, the delayed 2025 Federal Budget outlined a plan to increase the carbon tax at the industrial level to $170 per tonne by 2030.

The combination of rising corporate taxes, which will have to be passed along to consumers, and the elimination of the ‘year-over-year’ effect of the reduction of the consumer carbon tax will heavily influence overall inflation over the next six months. Further, the statistics agency continues to highlight the uncertainty over tariffs and their embedded influence on consumer prices going forward. The three Bank of Canada core inflation measures remained elevated in October, ranging from 2.7% to 3.0%. Any material resurgence in broader inflation would be viewed as sufficient rationale for the Bank of Canada to end the current cycle of lowering interest rates.

U.S. markets well ahead on first anniversary of presidential election

A contentious U.S. presidential election on November 5, 2024, was followed by a series of dramatic international developments in global trade and commerce. Nevertheless, while it has been a bumpy ride, the U.S. equity market has turned in an extraordinary performance over the past 12 months. After an initial move to a new high on February 19, the benchmark S&P 500 saw a correction that took the index back down 18.9% by the close on April 8. Still, this down-beat was fully recovered by June 27.

Eventually the index reached a new all-time, inter-day high of 6,920.3 on October 29, 2025. This level marked a 21.1% advance from the closing level established the day before the election and a cumulative 92.6% advance from the end of the bear market on October 12, 2022, seen during the previous administration.

Longer View

Hundreds of billions of dollars have been invested in artificial intelligence with the goal of boosting productivity, enhancing quality of life, and improving health outcomes. These investments are poised to yield tangible benefits beginning in 2026, with positive impacts expected to unfold over the next decade.

As with any transformative shift, the early stages may bring discomfort and disruption. However, through thoughtful adaptation and strategic modifications, the advantages of AI integration will become increasingly clear. AI has the potential to reshape industries and daily life alike. Crucially, the productivity gains driven by AI should help ease labour inflation pressures and support stronger earnings growth.

As businesses become more efficient and individuals more empowered, the long-term economic and societal benefits could be profound.

Important Disclaimers

The information contained herein consists of general economic information and/or information as to the historical performance of securities, is provided solely for informational and educational purposes and is not to be construed as advice in respect of securities or as to the investing in or the buying or selling of securities, whether expressed or implied. This document may contain forward-looking statements. These statements reflect what the authors believe and are based on information currently available to them. Forward-looking statements are not guarantees of future performance. We caution you not to place undue reliance on these statements as a number of factors could cause actual events or results to differ materially from those expressed in any forward-looking statement, including economic, political and market changes and other developments. Neither CI Private Wealth nor its affiliates, or their respective officers, directors, employees or advisors are responsible in any way for any damages or losses of any kind whatsoever in respect of the use of this document or the material herein. CI Private Wealth is a division of CI Private Counsel LP CI Assante Wealth Management is a registered business name of Assante Wealth Management (Canada) Ltd. CI GAM | Multi-Asset Management is a division of CI Global Asset Management. CI Global Asset Management is a registered business name of CI Investments Inc. This document may not be reproduced, in whole or in part, in any manner whatsoever, without the prior written permission of CI Private Wealth. © 2025 CI Private Wealth, a division of CI Private Counsel LP. All rights reserved. 25-10- 1517800 (10/25)