June 2025 Portfolio Construction

By Alfred Lam, CFA, Senior Vice-President, and Co-Head of Multi Asset, CI Global Asset Management and Richard J. Wylie, MA, CFA, Vice-President, Investment Strategy of CI Assante Wealth Management.

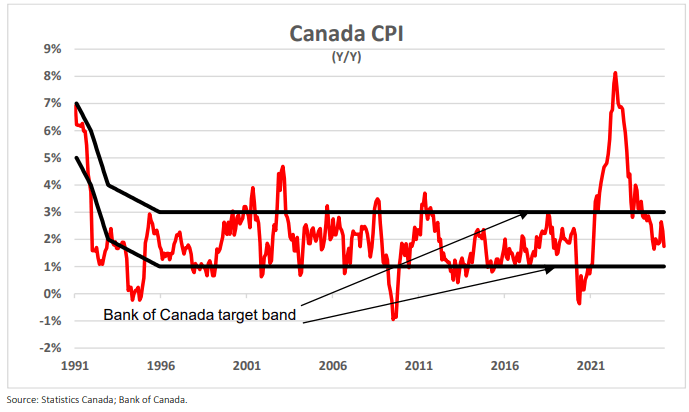

Canadian inflation falls on carbon tax cut

Carbon tax break lowers Canada’s inflation rate, for now

The latest data from Statistics Canada revealed that its Consumer Price Index fell 0.2% (seasonally adjusted) in April. On a year-over-year basis, the CPI was up 1.7%, a dramatic slowing from the 2.3% pace posted in March. As can be seen in the accompanying graph, this was the sixteenth consecutive monthly reading inside the Bank of Canada’s 1%–3% target band. Not surprisingly, the decline was led by energy prices, and the move coincided with the temporary reduction of the federal carbon tax.

The statistics agency explicitly stated that “gasoline led the decline in consumer energy prices, falling 18.1% year over year in April, following a 1.6% decline in March. The price decrease in April was mainly driven by the removal of the consumer carbon price. Year over year, prices for natural gas fell 14.1% in April, after a 6.4% gain in March. The removal of the consumer carbon price contributed to the decline in April.” The influence of the tax reduction will take longer to work through other components of the CPI “basket of goods”. Food (+3.8% year-over-year) and shelter (+3.4%) continue to show the greatest upward momentum. On a longer, five-year basis, these two components are up 43.3% and 21.4%, respectively.

Considerable uncertainty remains over tariffs and their influence on consumer prices going forward. The market will, once again, assess the chances of another rate cut by the Bank of Canada at the June 4 policy announcement.

U.S. labour market remains firm

The U.S. Bureau of Labor Statistics announced that the unemployment rate was unchanged in April, matching the 4.2% level reported in March. At the same time, non-farm payroll gains were reported as 177,000 during the month, adding to the revised 185,000 gain posted for March (originally reported as 228,000). This advance in employment takes the streak of uninterrupted gains to 52 months.

During April, average hourly earnings also climbed 0.2%, a 49th consecutive gain. Hourly earnings now stand with a year-over-year advance of 3.8%. This is well above headline inflation (2.4% in March). The strength of this report will prompt further market debate on the probability that the Fed will remain “on hold” at their pending policy meeting, scheduled for June 17 and 18, 2025.

Impact of Trump’s Tariff Proposal on Geopolitics and Global Trade

1. Disruption of Global Supply Chains

The push to “buy American” and for “made in America” products aims to bring manufacturing and sourcing back to U.S. soil. It

fundamentally disrupts the global supply chains that have been optimized over decades by business owners with little influence

by governments. These disruptions could result in:

- Higher input costs for U.S. manufacturers relying on foreign components and labour.

- Delays in production cycles due to the restructuring of sourcing networks.

- Retaliatory tariffs from trade partners, escalating into broader trade wars.

2. Inflationary Pressures

With new tariffs, fewer cheap imports, and rising production costs, inflation is likely to rise. Higher inflation, without

corresponding wage growth or productivity gains, could:

- Erode consumer purchasing power.

- Prompt the Federal Reserve to raise interest rates faster, potentially stifling investment and borrowing.

3. De-Globalization and Strategic Withdrawal

U.S. companies have long benefited from globalization, accessing cheaper labor, broader markets, and more diverse supply chains. A move toward de-globalization could:

- Undermine the competitive advantage of U.S. multinational corporations.

- Lead to loss of market share to more trade-flexible competitors (e.g., EU or Chinese firms).

- Diminish the U.S.’s role in shaping global trade norms and standards.

4. Impact on the U.S. Dollar and Financial Markets

The U.S. dollar and Treasury markets are underpinned by:

- Confidence in the U.S. economic model.

- Global dependence on the dollar for trade and reserves. If the U.S. appears to be turning inward, that could shake longstanding trust:

- Demand for U.S. assets like Treasuries could weaken.

- The valuation premium of U.S. equity markets could decline.

- Long-term investors might reallocate capital to emerging markets or regions with a more stable and open trade outlook.

Disclaimers

The information contained herein consists of general economic information and/or information as to the historical performance of securities, is provided solely for informational and educational purposes and is not to be construed as advice in respect of securities or as to the investing in or the buying or selling of securities, whether expressed or implied. This document may contain forward-looking statements. These statements reflect what the authors

believe and are based on information currently available to them. Forward-looking statements are not guarantees of future performance. We caution you not to place undue reliance on these statements as a number of factors could cause actual events or results to differ materially from those expressed in any forward-looking statement, including economic, political and market changes and other developments. Neither CI Private Wealth nor its affiliates, or their respective officers, directors, employees or advisors are responsible in any way for any damages or losses of any kind whatsoever in respect of the use of this document or the material herein. CI Private Wealth is a division of CI Private Counsel LP CI Assante Wealth Management is a registered business name of Assante Wealth Management (Canada) Ltd. CI GAM | Multi-Asset Management is a division of CI Global Asset Management. CI Global Asset Management is a registered business name of CI Investments Inc. This document may not be reproduced, in whole or in part, in any manner whatsoever, without the prior written permission of CI Private Wealth. © 2024 CI Private Wealth, a division of CI Private Counsel

LP. All rights reserved. 25-05-1361571(05/25)