May 2026 Portfolio Construction

By Alfred Lam, CFA, Senior Vice-President, and Co-Head of Multi Asset, CI Global Asset Management and Richard J. Wylie, MA, CFA, Vice President, Investment Strategy, CI Assante Wealth Management

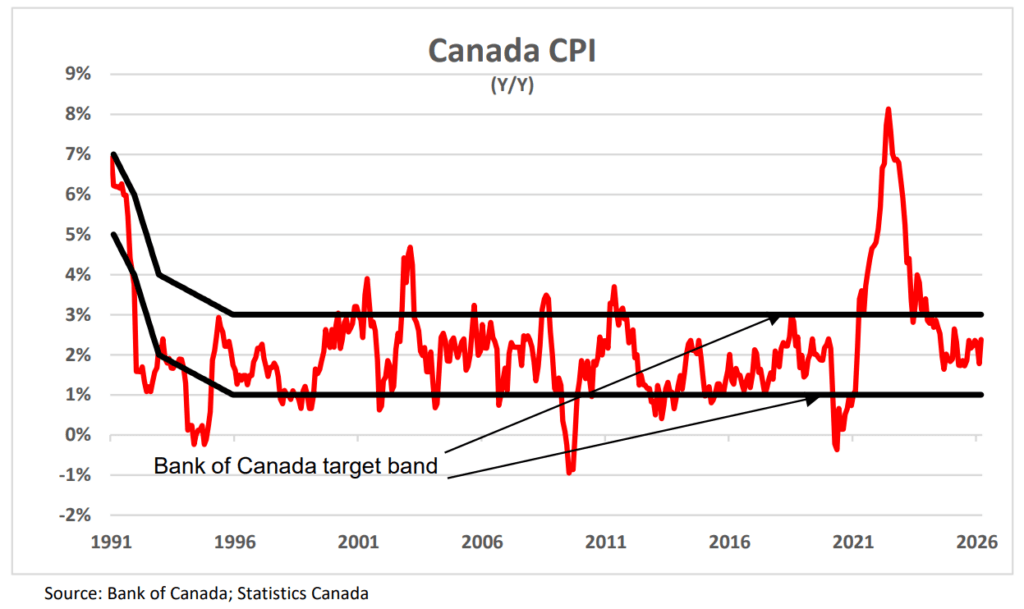

Canadian inflation remains contained, despite energy price surge

Gasoline prices fuel inflationary increase

The latest inflation report from Statistics Canada stated that gasoline “prices surged 21.2% on a monthly basis (March 2026), the largest price increase for gasoline on record, due to the supply shock resulting from the conflict in the Middle East.” Understandably, this advance helped to push the overall Consumer Price Index (CPI) up by 0.5% (seasonally adjusted) during the month. On a year-over-year basis, inflation rose to 2.4% from the 1.8% figure that was reported in February. As can be seen in the accompanying graph, despite this acceleration, inflation remains within the Bank of Canada’s 1% to 3% target band. While this is welcome news, consumers continue to deal with the fallout of the spike in the CPI seen in 2022 when inflation hit 8.1%, a fortyyear high. During the five-year period between March 2016 and March 2021 the CPI rose a cumulative 9.1%. Over the past five years it has increased more than twice as quickly (19.9%). Notably, cumulative gains in both food (7.6% to 29.6%) and shelter (11.3% to 26.7%) reflect the same acceleration trend. Not surprisingly, consumer concerns over affordability remain, despite the subdued headline CPI figures.

U.S. markets move to new highs

After making steady gains for the final three quarters of 2025, the benchmark S&P 500 closed at a new all-time high of 6,978.6 on January 25, 2026. Subsequently, the renewal of concerns over tariff-driven trade disputes bolstered selling pressure in equities throughout most of February. Further, the launch of “Operation Epic Fury” jointly by the U.S. and Israel on February 28 fostered considerable global uncertainty and dramatically increased inflationary fears. Selling pressure took the index close to “correction” territory (generally, a market decline of 10% is deemed to be a correction, while a bear market is widely recognized as a decline of 20% or more) as the index closed trading at 6,343.7 on March 30, down 9.1% from the peak. Regardless, the de-escalation of the Iran conflict and the reopening of the Strait of Hormuz for shipping produced a ‘V-shaped’ recovery in equity markets. The S&P 500 closed above technical resistance at the 7,000 level for the first time ever on April 15.

Longer View

In the near term, investor sentiment remains constrained by escalating geopolitical tensions stemming from the U.S.–Israel–Iran conflict. These developments have driven a sharp rise in oil prices, reigniting inflation expectations and increasing uncertainty across global markets. However, looking beyond this tragic and destabilizing episode, the medium- to longer‑term outlook remains constructive. Economic growth and corporate earnings should be supported by increasingly accommodative central bank policies as inflation pressures eventually normalize. At the same time, productivity gains driven by the next phase of the Industrial Revolution—led by rapid advancements and widespread adoption of artificial intelligence—have the potential to meaningfully enhance efficiency, profitability, and long‑term growth prospects across sectors.

Important Disclaimers

The information contained herein consists of general economic information and/or information as to the historical performance of securities, is provided solely for informational and educational purposes and is not to be construed as advice in respect of securities or as to the investing in or the buying or selling of securities, whether expressed or implied. This document may contain forward-looking statements. These statements reflect what the authors believe and are based on information currently available to them. Forward-looking statements are not guarantees of future performance. We caution you not to place undue reliance on these statements as a number of factors could cause actual events or results to differ materially from those expressed in any forward-looking statement, including economic, political and market changes and other developments. Neither CI Private Wealth nor its affiliates, or their respective officers, directors, employees or advisors are responsible in any way for any damages or losses of any kind whatsoever in respect of the use of this document or the material herein. CI Private Wealth is a division of CI Private Counsel LP CI Assante Wealth Management is a registered business name of Assante Wealth Management (Canada) Ltd. CI GAM | Multi-Asset Management is a division of CI Global Asset Management. CI Global Asset Management is a registered business name of CI Investments Inc. This document may not be reproduced, in whole or in part, in any manner whatsoever, without the prior written permission of CI Private Wealth. © 2025 CI Private Wealth, a division of CI Private Counsel LP. All rights reserved. 26-04-1764500 (04/26)