July 2025 Portfolio Construction

By Alfred Lam, CFA, Senior Vice-President, and Chief Investment Officer, CI GAM Multi-Asset Management and Richard J. Wylie, MA, CFA, Vice-President, Investment Strategy of CI Assante Wealth Management.

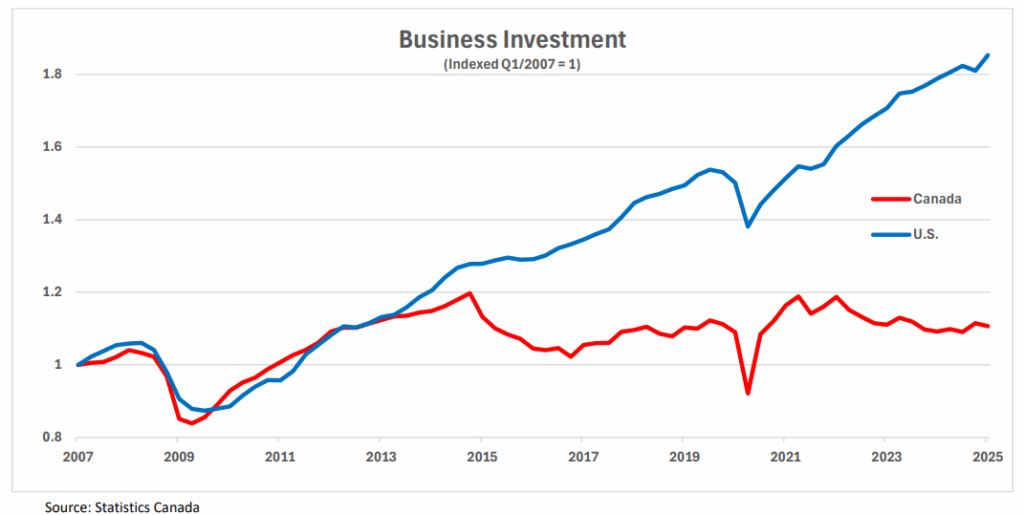

Canada–U.S. investment gap widens

Domestic investment falls again

Updated figures from Statistics Canada revealed that, while the broader economy expanded by 2.2% (annualized) during the first quarter of 2025, business investment contracted 3.1%. Stateside, business investment grew 9.8% in the first quarter (on the same basis). Much of Canada’s secular decline in productivity can be traced to the growing disparity in business investment between Canada and the U.S. Without investment in plants, machinery, and technology, Canadian workers are simply not given the same tools and have no chance to match their U.S. rivals in terms of output. This investment gap became most pronounced starting ten years ago.

Over the past decade, there has been broad intent to leave resources in the ground. Further, frequent and unpredictable changes in legislation and regulations have emerged. The volatile and often hostile government regulatory environment in Canada has left little appetite for domestic business investment. As can be seen in the accompanying graph, growth in overall business investment in Canada largely followed the pattern seen in the U.S. from before the Global Financial Crisis (GFC) through 2014.

However, this changed dramatically in 2015 with the new, incoming federal government. In fact, business investment has now fallen back to the same level seen in early 2012 and employment conditions are following. In May, Canada’s unemployment rate moved up to 7%, the highest since September 2021. Despite the ongoing trade issues, the Bank of Canada may become more focused on the domestic economy and policy implications at its upcoming July 30 interest rate announcement window.

U.S. consumers hit the brakes

The U.S. Bureau of Labor Statistics announced that retail and food services sales plummeted 0.9% (seasonally adjusted) in May. This was the largest single month decline since March 2023 and followed a revised 0.1% drop (previously reported as a 0.1% gain) in April. The recent move came as consumers stepped back from the advances made in March as the surge buying, seen ahead of the implementation of trade tariffs, has now dried up. Regardless of the decline, the recent volatility in overall sales has masked an underlying weakening trend in spending. During the first quarter of 2025, retail spending rose an annualized 1.6%. Spending is now on track to fall below that pace to an estimated 1.3%. Since consumer spending accounts for roughly two-thirds of U.S. economic activity, it is critical to overall GDP results. The current state of consumer spending will prompt further market debate on the direction that the Fed will take with respect to monetary policy.

Longer view

The global economic landscape became more complicated in April when President Trump followed through on his promise to impose new tariffs on imports to the U.S. While the announcement was anticipated, the specific tariff rates were not, sparking a four-day selloff that sent the S&P 500 Index down 12%. Acting as a voting machine, capital markets exerted enough pressure to prompt the administration to reconsider. Ultimately, a 90-day negotiation period was granted following four business days of market turmoil. Looking out longer, last year’s top investment theme—artificial intelligence—faced some turbulence.

Expectations that the launch of DeepSeek in China would shift the AI landscape were tempered as major U.S. tech firms like Microsoft, Meta, and Alphabet announced expanded capital expenditure plans. Sovereign wealth funds are now expected to overtake hyper scalers as the largest investors in data centers over the next two years. Meanwhile, adoption of agentic AI platforms such as ChatGPT and Meta AI continues to grow. Looking ahead, the next major AI frontiers are likely to be full self driving technology and humanoid robotics. Full self-driving is already being implemented and is expected to evolve into a smartphone-like ecosystem. By 2035, it’s anticipated that both factories and households will commonly utilize humanoid robots. We believe we are still in the early stages of what will be a long and transformative trend in AI.

Important Disclaimers

The information contained herein consists of general economic information and/or information as to the historical performance of securities, is provided solely for informational and educational purposes and is not to be construed as advice in respect of securities or as to the investing in or the buying or selling of securities, whether expressed or implied. This document may contain forward-looking statements. These statements reflect what the authors believe and are based on information currently available to them. Forward-looking statements are not guarantees of future performance. We caution you not to place undue reliance on these statements as a number of factors could cause actual events or results to differ materially from those expressed in any forward-looking statement, including economic, political and market changes and other developments. Neither CI Private Wealth nor its affiliates, or their respective officers, directors, employees or advisors are responsible in any way for any damages or losses of any kind whatsoever in respect of the use of this document or the material herein. CI Private Wealth is a division of CI Private Counsel LP CI Assante Wealth Management is a registered business name of Assante Wealth Management (Canada) Ltd. CI GAM | Multi-Asset Management is a division of CI Global Asset Management. CI Global Asset Management is a registered business name of CI Investments Inc. This document may not be reproduced, in whole or in part, in any manner whatsoever, without the prior written permission of CI Private Wealth. © 2024 CI Private Wealth, a division of CI Private Counsel LP. All rights reserved. 25-06-1393800(06/25)