September 2025 Portfolio Construction

Alfred Lam, MBA, CFA, Senior Vice-President & Chief Investment Officer, CI GAM | Multi-Asset Management

Richard J. Wylie, MA, CFA, Vice-President, Investment Strategy, CI Assante Wealth Management

Canada’s distorted jobs data

The latest figures from Statistics Canada revealed that overall employment plunged by 40,800 in July. However, these job losses come on the heels of an 83,100 gain reported for June. The combined results left annual job growth at 1.5%, below the 1.9% average in 2024 but above the 1.3% figure posted as recently as April 2025. At the same time, the unemployment rate held steady at 6.9% in July. On the surface, these figures appear respectable and could even be construed as reflecting a firm, or at least stable, labour market.

Unfortunately, this is not the case. The headline employment figures mask several secular trends that point to material underlying weakness in the domestic job market. A number of substantial changes to population, participation, inflation, expansion of the government, and the decline in Canada’s competitiveness with the U.S. have all played a role in the erosion of the labour market. Canada’s population surged from 35.8 million at the end of 2015 to 41.5 million during the first quarter of 2025.

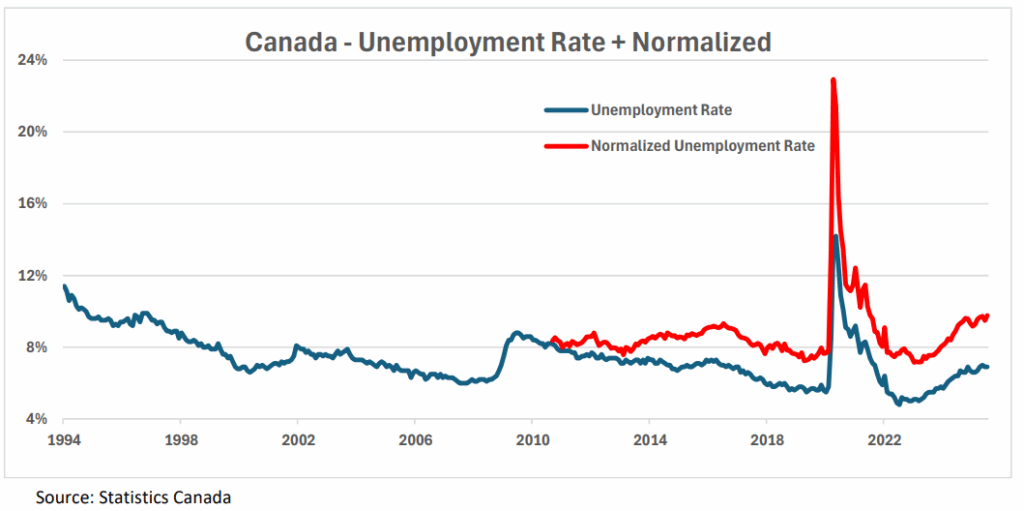

Unfortunately, jobs for all of these new Canadians have not yet been created. The participation rate (the percentage of working age individuals who were either working or looking for work) fell to 65.2%, far below the pre-pandemic peak of 67.3% observed in August 2010. The surge in the number of new Canadians that has accompanied this decline in participation has had a knock-on effect. The number of potential workers who are sitting on the sidelines has grown from 95,000 at the end of 2010 to 707,000 in the latest figures. Not surprisingly, as can be seen in the accompanying graph, the reported unemployment rate has been distorted as a result. A return to 67.3% participation would produce a more realistic unemployment rate of 9.8%, a level not seen – excepting the COVID-19 lockdown – since November 1996 (9.9%). This rate is, historically, consistent with a recession.

U.S. inflationary pressures edge higher

The U.S. Bureau of Labor Statistics reported that the consumer price index rose 0.2% (seasonally adjusted basis) in July, following a 0.3% June advance. Over the last 12 months, the overall index has increased 2.7%, matching the pace posted in the previous report. The current data also revealed that core inflation (CPI ex food and energy) rose 3.1% (y/y) in July, above the 2.9% pace seen in June. Inflation has eased considerably since hitting 9.1% in June 2022, which was its fastest annual pace since November 1981 (9.6%). Still, this report continues to show a mild increase in inflationary pressures since lows of 2.3% for overall inflation and 2.8% for core inflation were hit in April. The market will remain focused on the Fed’s pending two-day policy meeting scheduled for September 16 and 17.

The longer view

Investor attention has been focused on global tariffs initiated by President Donald Trump. While this is a significant development, it is unlikely to have the same long-term impact as innovation on our lifestyle, economy, and stock market performance over the next decade. Artificial intelligence will not only strengthen existing ecosystems but also has the potential to create entirely new ones. In a rapidly changing world, the most dangerous investment strategy is one based on a “rear-view mirror” mindset.

Important Disclaimers

The information contained herein consists of general economic information and/or information as to the historical performance of securities, is provided solely for informational and educational purposes and is not to be construed as advice in respect of securities or as to the investing in or the buying or selling of securities, whether expressed or implied. This document may contain forward-looking statements. These statements reflect what the authors believe and are based on information currently available to them. Forward-looking statements are not guarantees of future performance. We caution you not to place undue reliance on these statements as a number of factors could cause actual events or results to differ materially from those expressed in any forward-looking statement, including economic, political and market changes and other developments. Neither CI Private Wealth nor its affiliates, or their respective officers, directors, employees or advisors are responsible in any way for any damages or losses of any kind whatsoever in respect of the use of this document or the material herein. CI Private Wealth is a division of CI Private Counsel LP CI Assante Wealth Management is a registered business name of Assante Wealth Management (Canada) Ltd. CI GAM | Multi-Asset Management is a division of CI Global Asset Management. CI Global Asset Management is a registered business name of CI Investments Inc. This document may not be reproduced, in whole or in part, in any manner whatsoever, without the prior written permission of CI Private Wealth. © 2025 CI Private Wealth, a division of CI Private Counsel LP. All rights reserved. 25-08- 1431349(08/25)